This is educational content, not financial advice.

Artificial intelligence isn’t just writing poems and debugging code—it’s quietly reshaping how money is managed. AI investing uses algorithms to analyze markets, manage risk, and automate decisions that used to require a room full of analysts. For beginners and busy professionals in the US and UK, AI can lower costs, reduce guesswork, and add discipline to your portfolio. This guide explains what AI investing is, the main tools available, the risks to watch, and a practical step-by-step plan to get started responsibly.

Table of Contents

What Is AI Investing?

AI investing refers to using machine-learning models and data-driven algorithms to select, weight, rebalance, and risk-manage investments. This includes:

- Robo-advisors that build and manage diversified portfolios automatically.

- Factor and smart-beta strategies enhanced by AI signals (e.g., momentum, quality).

- Algorithmic trading that executes rules at machine speed.

- Alternative data analysis (news, earnings calls, satellite images) processed by natural-language and computer-vision models.

- Risk models that adjust allocations when volatility spikes.

AI isn’t a crystal ball. It’s a tool for pattern detection, probability, and disciplined execution. Your job is to set goals, risk limits, and guardrails.

AI investing draws on machine-learning models to analyze markets, automate rebalancing, and manage risk. For a neutral primer on ETFs and diversification, see the U.S. SEC’s guide to Exchange-Traded Funds (ETFs) and the UK FCA’s InvestSmart initiative for retail investors.

Why AI? The Practical Advantages

1) Discipline without drama

Algorithms don’t panic on red days or get euphoric on green days. That alone can improve long-term outcomes for many investors.

2) Lower costs at baseline

Robo-advisors and index-first AI strategies often charge a fraction of traditional management fees.

3) Diversification by default

Most consumer AI platforms start with broad ETFs across stocks/bonds/cash, then optimize.

4) Faster research

AI can scan thousands of securities, earnings transcripts, and macro signals in minutes—useful for filtering ideas you then evaluate.

5) Personalization

Many tools let you set a target risk level, include/exclude sectors (e.g., energy, defense), or add sustainability screens.

Where AI Shows Up in Everyday Investing

1) Robo-Advisors (Hands-Off, Goal-Based)

Robo-advisors ask about your horizon, risk tolerance, and income needs. They recommend a diversified ETF portfolio and automate deposits, tax-loss harvesting (US), and rebalancing. Some offer responsible investing screens.

Best for: New investors, time-poor professionals, those who want automated discipline.

2) AI-Enhanced ETF Strategies

Index funds remain the core, but some ETFs use AI to tilt weights toward factors (quality, value, momentum) or to screen news sentiment. Treat these as satellite positions around a diversified core, not as all-in bets.

Best for: Intermediate investors who want a modest edge without managing positions daily.

3) Rules-Based or Algorithmic Trading

Predefined rules (e.g., moving-average crossovers, volatility filters) can be automated via brokers or third-party tools. Some platforms provide AI-generated signals you can test. This is higher engagement and risk.

Best for: Hands-on learners comfortable with backtesting and strict risk controls.

4) Research Copilots

Large language models and specialized finance tools can parse earnings calls, summarise filings, and surface watchlist alerts—speeding up your due diligence while leaving final judgment to you.

Best for: Anyone who wants to research smarter, not longer.

The Risks (and How to Reduce Them)

AI won’t rescue a bad plan. Manage these risks:

- Model overfitting: A strategy that looked brilliant on past data may stumble live.

Mitigation: Prefer simple, transparent rules and long out-of-sample tests.

If you use backtests, incorporate trading costs and slippage and avoid curve-fitting. For U.S. taxable accounts, understand wash-sale rules before attempting tax-loss harvesting (see IRS Publication 550: Investment Income and Expenses). - Regime shifts: Markets change character (rates, inflation, geopolitics).

Mitigation: Diversify globally across assets; avoid single-signal dependence. - Hidden complexity: Black-box models can hide risk concentrations.

Mitigation: Use tools with clear documentation; understand what drives returns. - Over-trading and fees: Frequent trades can erode gains via spreads and taxes.

Mitigation: Favor low-turnover core holdings; be intentional with satellite strategies. - Latency and execution: In fast markets, fills may differ from backtests.

Mitigation: Add slippage and costs to tests; use limit orders when appropriate. - Behavioral risk: It’s easy to override systems at the worst time.

Mitigation: Precommit to rules and position sizes before emotions spike.

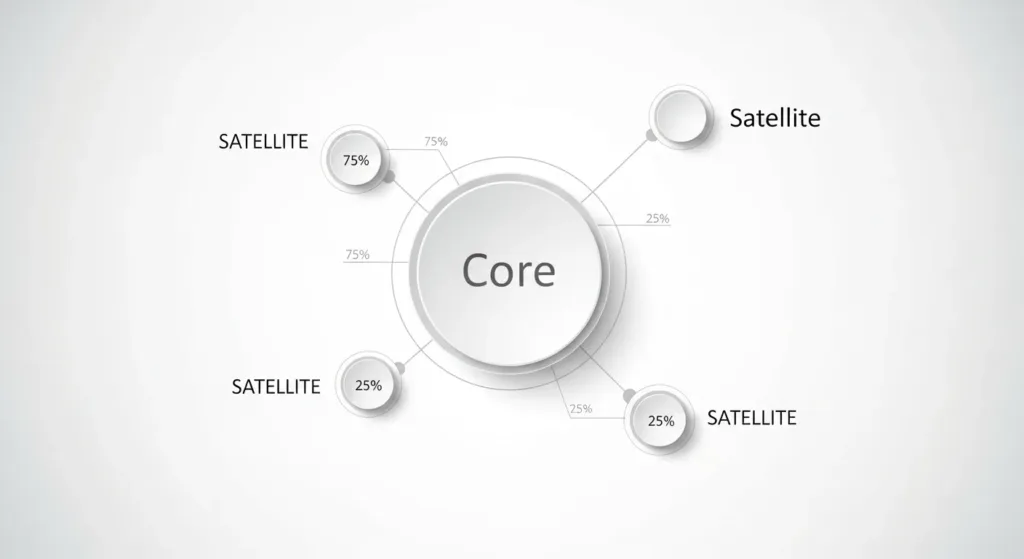

Core vs. Satellite: A Sensible Portfolio Structure

Think of your portfolio in two layers:

- Core (60–90%): Low-cost, diversified ETFs or a robo-advisor that uses AI for rebalancing and tax efficiency. Objective: market-level returns with minimal hassle.

- Satellite (10–40%): AI-tilted factors, thematic ETFs, or one or two rules-based strategies you understand. Objective: potential outperformance without endangering the whole plan.

This balance lets you benefit from AI while protecting against any single model’s failure.

Step-by-Step: How to Start with AI Investing

Step 1: Define your goals and constraints

- Goal examples: “Retirement in 25 years,” “House deposit in 5 years,” “Education fund in 10 years.”

- Constraints: minimum cash buffer, ethical exclusions, tax wrappers (ISA in the UK; IRA/401(k) in the US).

Start with a diversified core, then add a small satellite that you can explain in one sentence. The FCA’s InvestSmart and the SEC’s Investing Basics pages are excellent neutral references.

Step 2: Choose your primary route

- Hands-off: Select a reputable robo-advisor with transparent fees and diversified ETF portfolios.

- Hands-on: Choose a broker that supports automation, paper trading, and API access. Ensure good data quality and clear cost disclosures.

Step 3: Build your core

- Use broad ETFs covering US, international, and bonds. Many robo-advisors do this automatically.

- Set automatic monthly contributions (dollar-cost averaging) to smooth volatility.

Step 4: Add one satellite strategy (optional)

- Example: An AI-tilted factor ETF capped at 10–15% of portfolio.

- Or: A simple moving-average trend rule on a broad index ETF that goes to short-term Treasuries when the trend breaks. Backtest it; include trading costs and slippage.

Step 5: Risk management rules

- Max drawdown you can tolerate (e.g., 15–20%).

- Position sizing (e.g., 1–2% risk per trade for active strategies).

- Rebalance frequency (quarterly or semi-annual).

- A written “override policy” (when, if ever, you’ll turn a system off).

Step 6: Tax and account hygiene

- US: Consider tax-advantaged accounts (401(k), IRA). Some robo-advisors offer tax-loss harvesting in taxable accounts.

- UK: Use ISAs and pensions (SIPP) to shelter returns. Keep records of contributions and allowances.

Step 7: Review once per quarter

- Track allocations, fees, turnover, and slippage.

- Record what worked, what didn’t, and whether you followed your rules. The meta-discipline is the edge.

Key Terms Explained (Plain English)

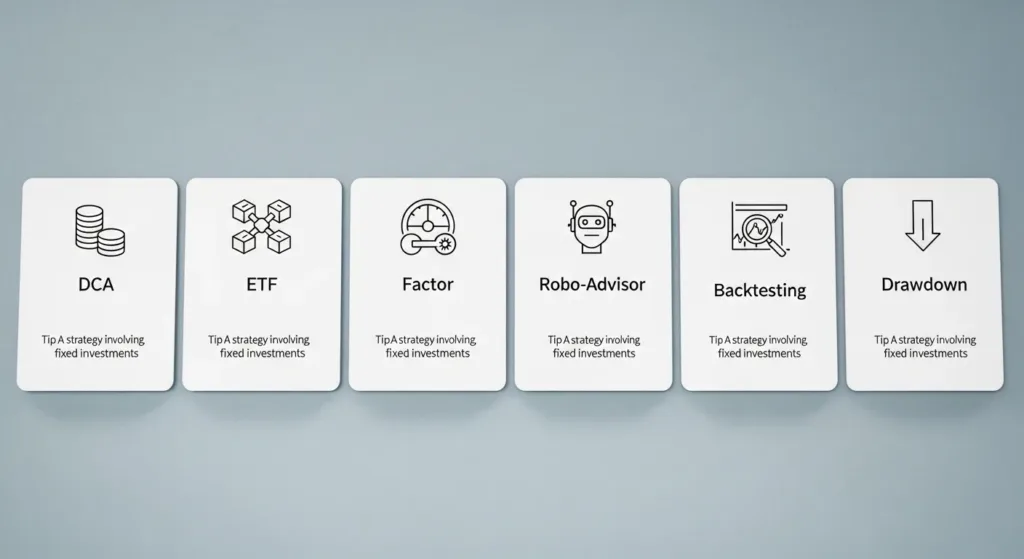

- Dollar-Cost Averaging (DCA): Investing a fixed amount at regular intervals. Reduces timing risk.

- ETF (Exchange-Traded Fund): A basket of securities you can buy like a stock, often low-cost and diversified.

- Factor Investing: Tilting a portfolio toward characteristics (value, quality, momentum) historically linked to returns.

- Robo-Advisor: An online platform that automates portfolio construction and management based on your goals and risk profile.

- Backtesting: Testing a strategy on historical data to estimate how it might have performed—useful but not predictive.

- Drawdown: The percentage decline from a portfolio’s peak to a subsequent low.

ETF: A pooled fund that trades like a stock. See the SEC’s overview of ETFs for risks, costs, and structures.

Pros and Cons of AI Investing

| Aspect | Pros | Cons |

|---|---|---|

| Costs | Often lower than traditional advice | Some advanced tools add subscription/data fees |

| Discipline | Removes emotion and enforces rules | Temptation to override during stress |

| Performance | Can surface edges from data signals | Overfitting and regime change can hurt |

| Effort | Automation saves time | Setup and monitoring still required |

| Transparency | Many robo-advisors are clear and simple | Black-box models may hide risks |

Common Mistakes to Avoid

- Chasing the newest model after a short period of outperformance.

- All-in bets on a single AI ETF or strategy.

- Ignoring taxes and fees in backtests.

- No contingency plan for severe market stress.

- Neglecting the core in favor of satellites that feel more “exciting.”

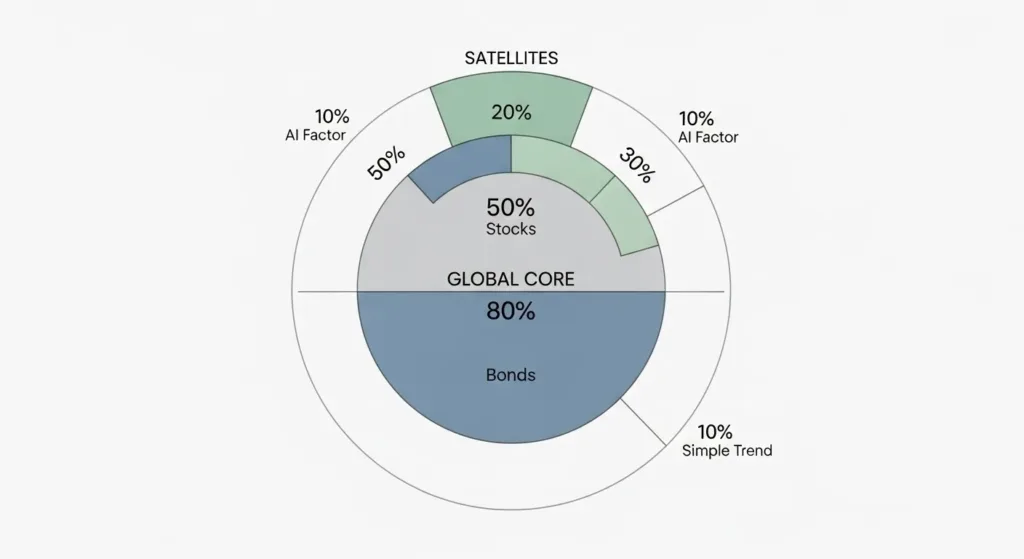

A Sample Beginner Set-Up (Illustrative Only)

- Accounts:

- US: 401(k)/IRA for core holdings; taxable account for satellites and TLH.

- UK: Stocks & Shares ISA/SIPP for core; taxable account for experimental slices.

- Core (80%):

- Global equity ETF(s) + investment-grade bonds, rebalanced semi-annually via robo-advisor or rules. Automatic monthly contributions.

- Satellite (20%):

- 10% AI-tilted factor ETF.

- 10% simple rules-based trend strategy on a broad index ETF with a cash/T-bill fallback.

- Controls:

- Max position per satellite fund: 10%.

- Quarterly check-in; halt any satellite that breaches drawdown rules.

Ethical and Sustainability Considerations

Many platforms support ESG or “responsible” screens. If avoiding certain sectors matters to you, enable these filters in your robo-advisor or ETF selection. Remember: exclusions can change risk/return; treat them as a preference you’re willing to carry.

Checklist Before You Press “Invest”

- Goals and timelines documented

- Emergency fund separate from investing

- Fees, bid-ask spreads, and taxes understood

- Written allocation with core vs. satellite weights

- Risk rules and rebalancing cadence set

- Paper-tested any algorithmic strategy with realistic costs

- Automation switched on; notifications enabled

Frequently Asked Questions

Is AI investing safe for beginners?

As safe as the underlying assets and your risk discipline. Start with a diversified robo-advisor or low-cost ETFs. Keep satellites small.

Will AI guarantee higher returns?

No. AI can improve process and consistency, but markets are uncertain. Treat any “edge” as probabilistic, not permanent.

What’s the minimum to begin?

Many robo-advisors and brokers have low or no minimums. Focus on consistent contributions rather than timing perfection.

How often should I tweak settings?

Quarterly reviews are enough for most. Constant tinkering often hurts.

Do I need coding skills?

Not for robo-advisors or AI-enhanced ETFs. Coding helps for custom strategies but isn’t required.

Conclusion: Let AI Do the Boring Work; You Do the Planning

AI is best at discipline, data scanning, and risk routines. You’re best at defining goals, setting boundaries, and sticking to a plan. Use AI investing to automate the mundane parts, keep a diversified core, and experiment thoughtfully at the edges.