Table of Contents

What Is Compound Interest? The Complete, Practical Guide for Savers, Investors, and Borrowers

(Educational only — not financial advice)

If you want money to quietly work while you sleep, you’re looking for the interest-on-interest effect. It’s the engine that lets small balances become meaningful sums, not through luck, but through math plus time. This guide shows how Compound Interest works, where you’ll see it in daily life, what slows it down, and how to build simple habits that keep the flywheel turning for years.

1) Compound Interest in One Minute (The Snowball Picture)

Imagine placing a snowball at the top of a long hill. Each rotation adds a thin layer of snow. At first, the ball looks unchanged. Then, seemingly out of nowhere, it’s bigger with every turn. Money can behave the same way when growth remains invested. First your balance earns a small return; next period you earn on the balance plus last period’s gain. Repeat, and the curve starts to bend upward.

A tiny example at 5% per year:

- End of Year 1: $100 → $105

- End of Year 2: $105 → $110.25

- End of Year 3: $110.25 → $115.76

That extra $0.76 by year three (versus simple, flat interest) is the effect beginning to show. Extend the timeline and the difference becomes less “tiny” and more “wow.”

2) Why Compound Interest Rewards Early, Consistent Contributions

Two truths drive the magic:

- Time is the multiplier. The longer your runway, the more dramatic the curve.

- Consistency beats intensity. Automated, modest contributions done relentlessly will often outpace irregular, larger deposits.

Consider two savers:

- Avery starts at 25, adds a fixed amount monthly for three decades.

- Blake delays a decade and contributes double each month for twenty years.

Despite the larger monthly number, Blake’s late start often finishes behind because Compound Interest had fewer years to work. The lesson is simple: start, even small. Your future self will thank you.

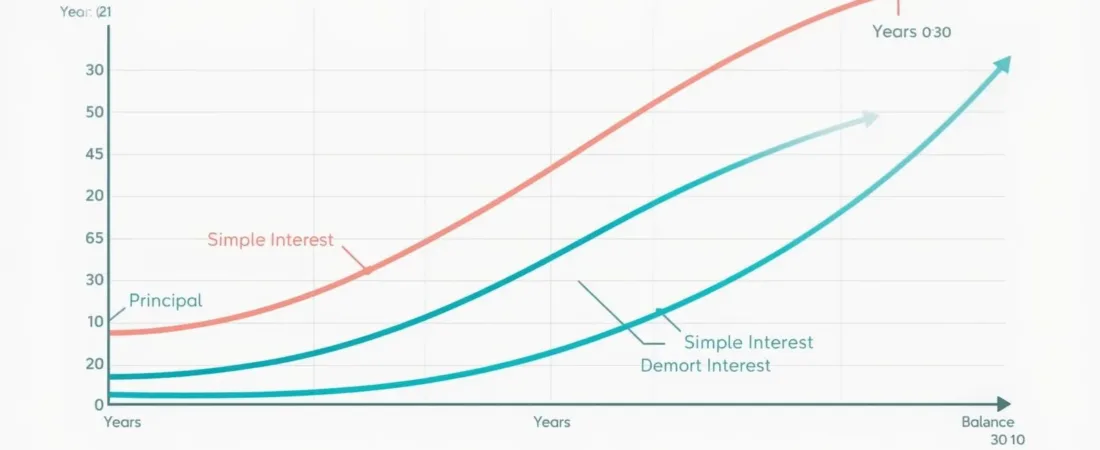

3) Simple vs. Compounding: What’s the Difference?

Only Compound Interest earns on past interest; that’s why the gap widens over time.

- Simple interest pays only on the original deposit (principal).

- Compound interest: you earn on principal and previously credited growth.

At 5% for three years on $1,000:

- Simple → $1,150 total

- Compounding → $1,157.63 (each year builds on a slightly larger base)

Over 10, 20, 30 years, Compound Interest becomes the whole story.

4) Compound Interest Formula (Peek—Apps Can Do It)

A=P (1+rn)n tA = P\,(1+\frac{r}{n})^{n\,t}A=P(1+nr)nt

- A = future value

- P = starting amount

- r = annual rate (decimal)

- n = number of credits per year (12 = monthly, 365 = daily)

- t = years

Example: $1,000 at 5% once per year for 3 years → $1,157.63.

You don’t need to memorize the formula. What matters is understanding the levers: time, rate, and how often growth is applied.

5) The Rule of 72: A Pocket Shortcut

To estimate doubling time, divide 72 by the rate (as a percentage):

- 6% → about 12 years

- 9% → about 8 years

It’s a rule of thumb, most accurate in the mid-single to low-double-digit range. Use it to gut-check expectations.

6) Frequency Matters (a Little)

Daily crediting boosts Compound Interest more than monthly or annual cycles.

All else equal, more frequent credits increase growth slightly:

- Annually → once per year

- Quarterly → four times

- Monthly → twelve times

- Daily → ~365 times

Banks often compute savings growth daily; investment platforms reinvest distributions when they arrive. The difference between monthly and daily isn’t massive, but over long spans every bit helps Compound Interest.

7) Match Time Horizon to Compound Interest Vehicles

0–2 years (safety first):

Short-term goals and emergency buffers belong in accounts designed for stability and liquidity. Predictability beats chasing yield.

3–10 years (balanced approach):

Blend assets so the curve can work while day-to-day swings don’t dominate your life.

10+ years (growth-leaning):

Give the engine room to run with more exposure to broad equity markets, paired with occasional rebalancing.

Matching time horizon → tool prevents forced selling and keeps the long-term plan intact.

8) Where You’ll See It in Real Life (US & UK)

Whether you use HYSAs or index funds, Compound Interest rewards consistency.

A) High-Yield Savings Accounts (HYSAs)

- US: Many online banks publish APY, which already reflects compounding.

- UK: Easy-access and fixed-term options may credit monthly or annually. Always check the details.

Perfect for buffers and near-term goals. Returns are steady and low-risk, though typically lower than long-run equity returns.

Try a calculator:

compound interest calculator (SEC Investor.gov)B) Broad Index Funds & ETFs (with reinvested distributions)

Reinvesting dividends buys more units, which then generate future payouts — a self-reinforcing loop. Over long spans, this can be a powerful source of growth thanks to market participation plus the interest-on-interest effect.

C) Tax-Advantaged Wrappers (they amplify results)

- US: 401(k), 403(b), IRA, Roth IRA. Employer matches are rare, high-impact boosts.

- UK: Workplace pensions and Stocks & Shares ISAs can shelter returns, letting more of each year’s gain remain invested.

D) The Dark Mirror: Credit Cards and High-APR Loans

The same mechanics can work against you. Carry a balance at a high rate and it can balloon quickly. Paying in full (or attacking the balance aggressively) stops the negative snowball before it grows teeth.

9) APR vs. APY: Know Your Acronyms

- APR (Annual Percentage Rate) shows the raw rate, typically on loans and cards; it doesn’t include the compounding effect.

- APY (Annual Percentage Yield) includes compounding and is used for savings and deposits.

Comparing savings products? Look at APY. Understanding borrowing costs? Look at APR and how often the lender updates the balance.

Helpful explainer:

APR basics (CFPB) and UK guide to compound interest (MoneyHelper).10) The Three Quiet Drags: Fees, Taxes, Inflation

Accounts like 401(k), IRA, ISAs let Compound Interest grow with fewer leaks.

- Fees: Expense ratios, platform charges, and advisory costs quietly siphon future dollars. A 1% annual drag is 1% of your future — every year. Favor low-cost choices.

- Taxes: Dividends, interest, and realized gains may be taxable. Wrappers (pensions, ISAs, 401(k)/IRAs) help keep more of each year’s growth at work.

- Inflation: Rising prices reduce purchasing power. Over long spans, growth assets help offset this; pair them with a cash buffer for near-term needs.

Reduce these frictions and the curve steepens without changing your effort.

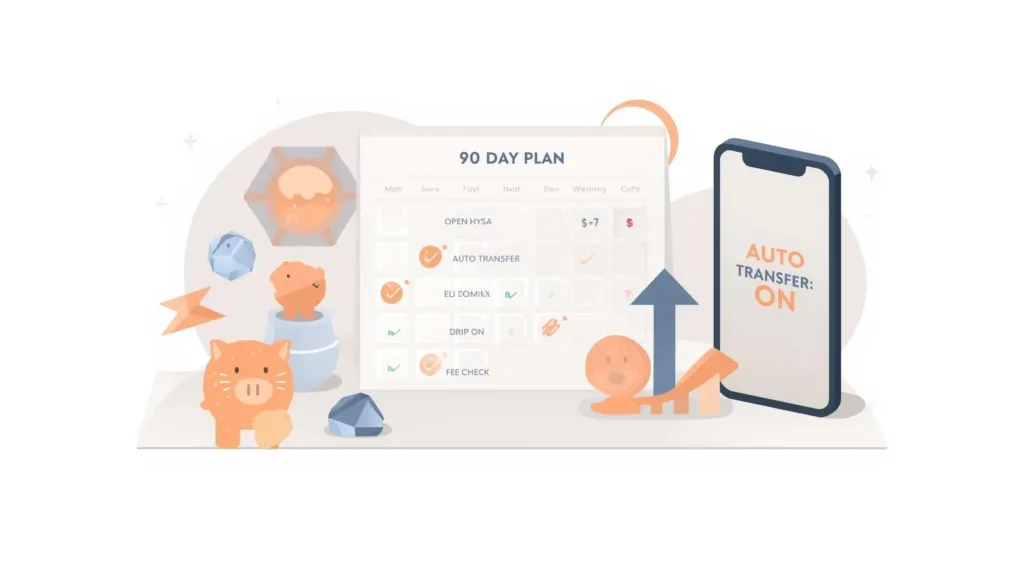

11) A 90-Day Action Plan (Small Steps, Big Momentum)

Automate deposits so Compound Interest starts working in the background.

Weeks 1–2

- Open a dedicated savings account for your buffer.

- Open or confirm an investing account (workplace pension/401(k)/ISA/IRA or a low-cost brokerage).

- Automate two transfers: one to savings, one to investing, scheduled the day after payday.

Weeks 3–4

- Turn on distribution reinvestment (DRIP) where available.

- Choose one or two broad, low-cost index funds for long-term goals.

- Write down one short-term target and one long-term target; link each to an account.

Month 2

- Audit fees and shift to lower-cost options if possible.

- Capture any employer match (US) or ensure pension contributions are on track (UK).

- Keep the automation humming — habits feed the snowball.

Month 3

- Hit a first buffer milestone (e.g., $/£1,000).

- If comfortable, nudge contributions up by $/£10–25.

- Set two calendar reminders per year to review allocation and costs.

- Celebrate your streak — because sticking with it is the actual advantage.

12) Behavior Traps That Break the Flywheel

Lower expense ratios keep more Compound Interest compounding for you.

- Waiting to “have more.” The missed years cost more than small contributions help.

- Strategy hopping. Constantly changing lanes interrupts compounding and turns investing into a hobby.

- Panic selling. Market dips are normal; a diversified mix and a cash buffer protect your long-term plan.

- Fee blindness. High ongoing costs compound against you with the same relentlessness as gains compound for you.

Make a simple plan, automate it, and let boredom be your edge.

13) Visual Metaphors that Make It Stick

Credit-card APRs can turn Compound Interest into a fast-growing liability.

- Snowball on a hill: every rotation adds mass, leading to faster growth.

- Tree growth: seasons pass, roots deepen, branches spread — slow, then obvious.

- Staircase that widens: each “step” is bigger because the base is larger than last time.

Pick the image that resonates and return to it whenever headlines get loud.

14) US & UK Notes You’ll Actually Use

United States

- Savings: compare APY; frequent crediting helps a little.

- Retirement: 401(k)/IRA/Roth IRA — tax benefits plus potential employer money.

- Education: 529 plans — long runway plus tax advantages.

United Kingdom

- ISAs: interest, dividends, and gains can be sheltered, letting the curve work unhindered.

- Workplace pensions: employer contributions are an immediate boost.

- Fixed-term savings: check how and when interest is added to maximize the effect.

15) Case Studies (Realistic, Not Extreme)

Case 1: The New Saver with a Tight Budget

- Goal: build a buffer and begin investing.

- Action: $/£25 per week to savings; $/£25 per week to a broad index fund; enable DRIP.

- Why it works: two tiny automations build two habits — safety plus growth — without decision fatigue. Over a year, the routine itself becomes the asset.

Case 2: The Rebuilder with a High-APR Card

- Goal: stop the negative snowball while keeping the long game alive.

- Action: minimum buffer (e.g., $/£750), then aggressive payments to the highest APR balance; contribute just enough to capture any workplace match; resume regular investing after the card is defeated.

- Why it works: kills the costliest leak first, yet preserves long-term momentum.

Case 3: The Family with Two Timelines

- Goal: buy a home in three years and retire in twenty-plus.

- Action: down-payment cash in safe vehicles; retirement on auto-pilot into diversified funds; quarterly check-ins and annual rebalance.

- Why it works: each goal gets the right tool, avoiding the classic error of pulling from long-term investments during a bad market to fund short-term needs.

Case 4: The Late Starter

- Goal: build meaningful retirement capital starting at 45–50.

- Action: maximize tax-advantaged space, minimize fees, automate contributions, and avoid risky one-off “catch-up” bets; extend working years a bit if feasible.

- Why it works: discipline and cost control become the primary levers; even with fewer years, a consistent plan compounds better than sporadic leaps.

16) Checklists You’ll Actually Use

Daily (2–3 minutes)

- Glance at your spending app; note only outliers.

- Add non-essential temptations to a 24-hour list instead of buying now.

Weekly (10 minutes)

- Confirm automatic transfers posted (savings, investing, debt).

- Cancel one tiny recurring cost and redirect it.

Monthly (20–30 minutes)

- Log balances (cash, investments, debt) once.

- Celebrate one win; fix one leak.

- Ensure distributions are still set to reinvest.

Semiannual (30 minutes)

- Rebalance if your mix drifted.

- Review fees; switch to cheaper share classes if available.

- Revisit goals; adjust contributions by a small notch if comfortable.

17) FAQs (Clear and Straight)

- Clear, quick answers to help you use Compound Interest well.

Q: When will I actually notice growth?

A: Commonly after 3–5 years, more clearly after a decade. Early years feel slow; later years feel surprisingly fast.

Q: Is daily crediting better than monthly?

A: Slightly. Over long spans it adds up, but the biggest wins come from time, contributions, and low costs.

Q: Does this apply to debt?

A: Yes — and that’s why high-APR balances are dangerous. Attack them fast to stop the “snowball in reverse.”

Q: Should I wait until I can invest a lot?

A: No. Small and automated beats large and delayed, because lost years never come back.

Q: Do fees really matter on small accounts?

A: Absolutely. Today’s small account aims to become tomorrow’s large account; keep costs lean from day one.

Q: What if markets drop right after I invest?

A: Stick to your schedule. Lower prices let you buy more units; patience plus diversification lets the long-term curve do its job.

18) Simple vs. Compounding (At a Glance)

- Compounding: earnings can earn more; ideal for multi-year saving and investing; curve steepens with time.

- Simple: flat growth on principal only; common in short-term promos and some loans.

19) Quick Recap and a 10-Minute “Do This Next”

Recap

- The interest-on-interest effect is patient, predictable, and powerful when you give it time.

- Use the right account for the right timeline, automate transfers, reinvest distributions, reduce fees, and shelter growth from taxes where possible.

- Protect the long game with a cash buffer so you’re never forced to sell at the wrong moment.

10-Minute To-Do

- Open or confirm a high-yield savings account for your buffer.

- Turn on automatic transfers to savings and investing.

- Enable distribution reinvestment where available.

- Put a 6-month reminder in your calendar to review allocation and fees.

- Keep going — boring, automated, repeated steps are the edge most people never use.

Start small, start now—Compound Interest shows up for people who stay consistent.

Protect your time horizon, and Compound Interest will do the heavy lifting.

Reminder: This guide is educational and not financial advice. Your situation is unique; consider consulting a qualified professional before making major decisions.