Saving and Investing on Any Budget: A Practical, Human Guide

Table of Contents

Introduction: Why “Saving and Investing” Matters Right Now

When money feels tight, it’s tempting to think you must choose between saving or investing. In reality, saving and investing work best together as a system for stability and growth. Savings protect you from shocks; investments help your money compound. The mix you choose depends on your income, risk tolerance, time horizon, and life goals—but the engine is the same: steady contributions, smart choices, and time in the market, not market timing. If you’re just starting, saving and investing in small, consistent amounts beats waiting for the “perfect moment” that rarely arrives.

A strong emergency fund buffers stress and prevents high-interest debt when life hits. Parallel to that, a simple, low-cost investment plan lets compounding do the heavy lifting. Over months and years, saving and investing become less about intensity and more about habits. Your goal isn’t perfection; it’s momentum.

The Two Gears: What Saving Does, What Investing Does

Think of your money strategy as a two-gear mechanism. Cash savings are the shock absorber. Investments are the engine. Blend both, and saving and investing reinforce each other:

- Savings (“now and near”): Cash for emergencies and near-term goals. It lowers stress, helps you avoid expensive credit, and keeps essential bills covered.

- Investments (“later and larger”): Assets like index funds, ETFs, or retirement accounts that are designed to grow over years. This is where compounding amplifies small contributions. Over time, saving and investing together build optionality—more choices, fewer crises.

The key insight: if you only save, inflation erodes purchasing power; if you only invest, you can get forced to sell at a bad time. A blended approach to saving and investing helps you stay in control.

Start Here: A Simple 3-Layer Plan

A practical way to structure saving and investing is to use three layers:

- Buffer layer (cash): 1–3 months of essentials to start (ultimately 3–6).

- Growth layer (core index funds): Broad, low-cost exposure to the market, automated monthly.

- Flex layer (short-term goals): Cash-like tools (e.g., high-yield savings or short-duration funds) for things you’ll need within 1–3 years.

This three-layer map keeps saving and investing clean in your mind: cash for safety, funds for growth, and a flexible pocket for predictable expenses.

SMART Money: Goal-Setting That Actually Sticks

Vague goals (“I should save more”) collapse under daily pressure. Use SMART goals to make saving and investing concrete:

- Specific: “Build an emergency fund of $1,500.”

- Measurable: “$125 per paycheck.”

- Achievable: “I can free this amount by canceling two subscriptions.”

- Relevant: “A buffer reduces my credit-card stress.”

- Time-bound: “Hit $1,500 in 12 weeks.”

Write them down. Pin them somewhere visible. When goals are visible, saving and investing becomes a set of tasks, not a vague wish.

Budgeting Without the Burnout

Budgets fail when they’re too strict or too vague. Choose a method you’ll actually use to support saving and investing:

- 50/30/20: 50% needs, 30% wants, 20% saving/investing.

- 60/30/10 (tight budgets): 60% needs, 30% wants, 10% saving and investing at first—then nudge up.

- Pay-yourself-first: Move money to savings/investing right after payday; spend what’s left.

Automation is your friend. The more you automate saving and investing, the less willpower you need weekly.

Micro Wins: Micro-Investing and Round-Ups

If the idea of investing feels intimidating, begin tiny. Round-ups, micro-deposits, and $25–$50 weekly transfers turn saving and investing into a habit. Small moves do two things:

- They build the muscle of consistency.

- They give compounding time to work.

You’re not trying to “get rich quick.” You’re building a system that keeps saving and investing in motion, even on tough weeks.

Debt vs. Investing: What Goes First?

High-interest debt is a hair-on-fire problem; it usually beats any expected market return. Tackle it aggressively while keeping a small emergency buffer so you don’t ping-pong back into debt. Meanwhile, if your employer offers a retirement match, consider contributing at least to the match while you reduce debt. That way, saving and investing continue, but your expensive interest cost still declines.

For low-interest debt (like some student loans or mortgages), a hybrid approach can make sense: continue regular payments and maintain saving and investing in low-cost funds. Balance the math with your peace of mind.

Fees Eat Futures: Go Low-Cost

Costs compound just like returns. High expense ratios and trading fees quietly shrink your future. Prefer low-cost index funds and ETFs; stick to a simple lineup that supports saving and investing without drama. Two or three funds can give global diversification. Fancy is optional; simple is scalable.

When you minimize costs, saving and investing become more efficient—even when contributions are small.

Time in the Market > Timing the Market

Trying to guess the perfect entry point is a trap. Historically, staying invested beats jumping in and out. A fixed monthly contribution, through thick and thin, integrates saving and investing into your routine. On down months, you buy more shares; on up months, your balance rises. The discipline matters more than the day-to-day noise.

The Psychology: Habits Beat Hype

Markets swing; humans feel. A few behavior rules keep saving and investing steady:

- Name your accounts (e.g., “Safety Net,” “Freedom 2035”) to anchor purpose.

- Hide temptation: separate your savings/investing from your everyday checking.

- Track streaks, not balances. The win is keeping deposits flowing.

The calmer your behavior, the stronger your saving and investing become over years.

Emergency Funds That Actually Work

Aim for 3–6 months of essential expenses. If that number feels huge, stage it:

- Stage 1: $500–$1,000 “micro buffer” to stop small crises.

- Stage 2: 1 month.

- Stage 3: 3 months.

- Stage 4: 6 months if your income is variable.

Park it in a high-yield savings account. This keeps saving and investing separate: cash for safety, funds for growth.

Short-Term Goals Without Derailing Long-Term Plans

You’ll have near-term needs—travel, car repairs, moving costs. For those, use cash or short-term instruments; avoid taking equity risk on money you’ll need soon. Protect long-term saving and investing by fencing off short-term goals in their own bucket.

Core vs. Satellite: A Simple Portfolio Map

To keep saving and investing clear:

- Core (70–90%): Broad, low-cost stock/bond index funds.

- Satellite (10–30%): Only if needed—specific tilts (e.g., small-cap value), or a conservative cash/short-duration sleeve for flexibility.

Don’t overcomplicate. A simple core does most of the work. Your behavior finishes the job.

Risk That’s Real: Volatility vs. Goals

Risk isn’t just price swings; it’s failing to reach your goals on time. Match saving and investing to time horizons:

- Under 3 years: prioritize stability (cash/short duration).

- 3–10 years: blend stock/bond funds to dampen swings.

- 10+ years: lean more into equities for growth.

Rebalance once or twice a year. Small trims keep saving and investing aligned with your targets.

Taxes: Location, Location, Location

Account type matters. Tax-advantaged retirement accounts can accelerate saving and investing by deferring or reducing taxes. If you have access to such accounts, automate contributions. For taxable accounts, prefer tax-efficient funds. Little frictions add up; remove them early.

Inflation: Plan for the Silent Erosion

Inflation quietly reduces purchasing power. That’s why pure cash isn’t enough. The role of equities and other growth assets is to outpace inflation over time, while your cash buffers volatility. Balancing saving and investing helps you both sleep at night and preserve tomorrow’s buying power.

Automate the Boring, Celebrate the Milestones

Set up automatic transfers the day after payday:

- Emergency fund transfer.

- Investment account transfer.

- Debt overpayment (if any).

Then celebrate milestones—first $1,000 saved, first $5,000 invested, a 12-month contribution streak. Positive feedback keeps saving and investing fun enough to stick.

Tools You’ll Actually Use

- A basic budgeting app to see cash flow.

- Your bank’s scheduled transfers to automate saving and investing.

- Your broker’s auto-invest into low-cost index funds.

- A simple spreadsheet (optional) to log goals, balances, and dates.

Pick two or three you’ll open weekly. Tools only help saving and investing if you actually use them.

Case Study 1: The Starter

Profile: $2,400 monthly net income, rent-heavy budget, no savings.

Plan:

- Build a $1,000 buffer in 10 weeks ($100/week).

- After that, redirect $50/week to a low-cost index fund.

- Keep $25/week to finish the buffer up to 1 month of expenses.

Why it works: The buffer prevents setbacks. The weekly auto-invest starts compounding. Over a year, saving and investing become habit.

Case Study 2: The Rebuilder

Profile: Variable freelance income, credit-card debt at 22% APR.

Plan:

- Minimum viable buffer: $750.

- Debt snowball with every extra dollar; pause satellites.

- Contribute just enough to capture any retirement match.

- After the highest-interest card is gone, restore saving and investing contributions and rebuild the buffer to 3 months.

Why it works: Killing high interest frees future cash flow. The small retirement match keeps long-term compounding alive.

Case Study 3: The Family Plan

Profile: Two incomes, childcare, saving for a home in 3 years, retirement in 25 years.

Plan:

- Cash bucket for the down payment (short-term, low-risk).

- Automate retirement contributions monthly (long-term growth).

- Quarterly rebalance.

Why it works: Time-matching goals prevents cannibalizing long-term saving and investing for short-term needs.

Market Storms: How to Stay the Course

Downturns are when saving and investing earn their future returns. A few rules help:

- Don’t look daily; review monthly or quarterly.

- Keep contributing—even if you trim amounts temporarily.

- Revisit risk only if your time horizon or job security changed, not because headlines are loud.

- Remember: future gains are “born” during scary periods.

Common Pitfalls (and How to Dodge Them)

- All cash, forever: inflation risk. Blend saving and investing.

- All risk, no buffer: forced selling. Build cash first.

- Fee bloat: prefer low-cost funds.

- Overtrading: automate and leave it alone.

- Chasing hot tips: a plan beats a hunch.

Measuring Progress Without Obsessing

Track what you control: contribution streaks, percentage of income saved, and a simple net-worth snapshot each quarter. When you measure behaviors, saving and investing feel like wins you can repeat.

A Yearly Tune-Up That Takes an Hour

Once a year, run this checklist:

- Are your goals still SMART?

- Did your emergency fund target change?

- Are you at your target allocation? Rebalance.

- Can you increase automation by even $10–$25/month?

- Any fee creep in your funds or accounts?

Tuning beats rebuilding. This protects saving and investing with minimal effort.

Mindset: Enough Is a Strategy

Ambition is great; burnout isn’t. Aim for “good enough to keep going.” Sustainable saving and investing is about setting a pace you can hold through birthdays, bills, and busy seasons. If you need to reduce contributions for a month, do it—then resume. Consistency over intensity.

Frequently Asked Questions (Straight Answers)

1) I can only spare $25 a week. Is that pointless?

Not at all. Saving and investing are compounding games. $25 weekly is $1,300 a year before any growth. Automate it. Increase later when you can.

2) Should I build savings before I invest?

Build a small buffer first ($500–$1,000), then split new dollars between the buffer and a low-cost fund. That way, saving and investing both move forward.

3) What if markets drop after I buy?

They will—sometimes. Keep buying small amounts on a schedule. Over time, down prices become opportunities for saving and investing.

4) Which comes first, high-interest debt or investing?

High-interest debt first (after a tiny buffer). If available, contribute enough to capture any employer match, then attack the debt, then boost saving and investing.

5) How many funds do I need?

Often two or three low-cost index funds are enough: a broad stock fund, a bond fund, and (optionally) an international fund. Simple supports saving and investing.

6) How do I avoid quitting when progress feels slow?

Track streaks, not just balances. Celebrate monthly contributions. Share the goal with a friend. The routine is the result in saving and investing.

7) What about short-term goals like moving or a car?

Use cash/short-duration tools for 1–3-year goals, so you don’t derail long-term saving and investing during market dips.

8) Is dollar-cost averaging better than lump sum?

If you already have a lump sum, statistics often favor investing sooner. But for income earners, auto-contributions (DCA) make saving and investing effortless and less stressful.

9) Do fees really matter on small accounts?

Yes. A 1% fee is 1% of your future, every year. Low-cost is a pillar of saving and investing at any account size.

10) How much cash is too much?

Beyond your emergency fund and near-term goals, excess cash can drag long-term results. Redirect the surplus to saving and investing in your core funds.

Daily / Weekly / Monthly Checklists You’ll Actually Use

Daily (2–5 minutes)

- Glance at your spending app; note only outliers.

- Zero-effort rule: if a temptation pops up, add it to a 24-hour list instead of buying now.

- Quick gratitude note: one benefit your saving and investing will unlock (less stress, a trip, breathing room).

Weekly (10–15 minutes)

- Confirm auto-transfers posted (savings, investments, debt).

- Review upcoming bills; avoid late fees.

- One tiny optimization: cancel a $5–$15 expense you don’t love. Redirect it to saving and investing.

Monthly (20–30 minutes)

- Log balances (cash, investments, debt) in a simple sheet.

- Revisit one goal: still relevant? Any micro-increase to automation?

- Check expense ratios/fees aren’t creeping up.

- Celebrate: write down one win from saving and investing this month.

Advanced (Still Simple) Ideas

Buckets by Time Horizon

Create three buckets and label them by time:

- 0–12 months: cash only.

- 1–5 years: balanced mix; protect principal.

- 5+ years: growth-oriented.

This keeps saving and investing aligned to when you’ll need the money.

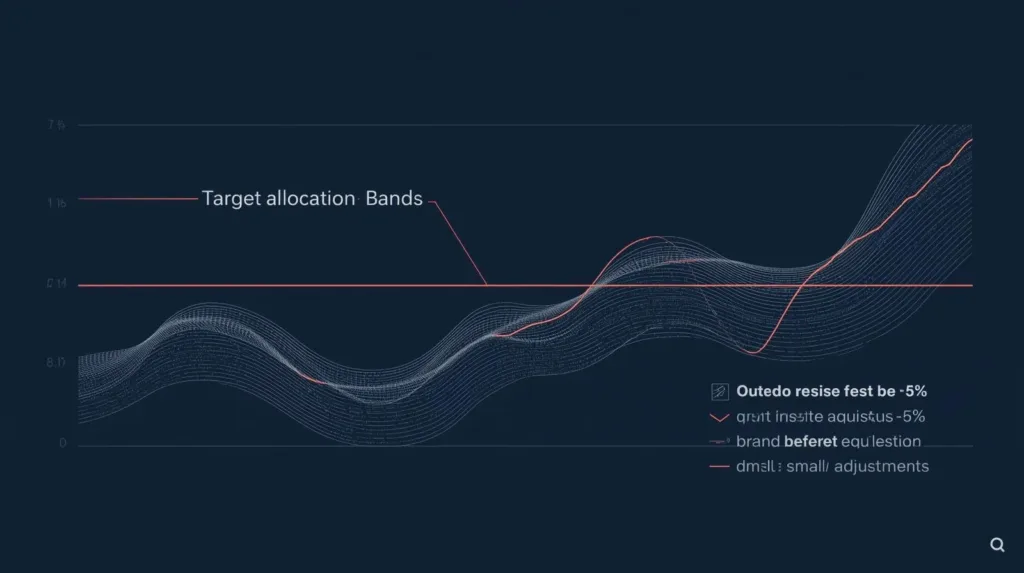

Rebalancing Bands

Instead of calendar-only rebalancing, add ±5% bands. If stocks drift above your target by 5%, trim a little to bonds (or vice versa). This keeps saving and investing close to plan without tinkering weekly.

Raise-Day Rule

Whenever your income rises, automatically boost contributions by a small percent. Let lifestyle lag your raises so saving and investing accelerate quietly.

Put It All Together: A 90-Day Action Plan

Week 1–2

- List essentials; set starter emergency target ($500–$1,000).

- Open a high-yield savings account and a low-cost brokerage/retirement account.

- Automate $25–$50 weekly to savings; $25–$50 to investments. Saving and investing begins.

Week 3–4

- Cancel/trim one recurring cost and redirect it.

- Name your accounts (“Safety Net,” “Future Me”).

- Write one SMART goal for each 90 days, 1 year, and 3 years.

Month 2

- Evaluate debt. If any APR > 15%, add a focused snowball.

- Keep contributions flowing; don’t pause saving and investing unless necessary.

- Learn one simple topic (asset allocation, fees, or taxes).

Month 3

- Hit starter buffer target; switch more dollars to investments.

- Set rebalancing rule (calendar or bands).

- Do a 30-minute review: what worked? What can you automate?

- Celebrate your streak—because saving and investing you actually do beats the perfect plan you never start.

Closing Thought: Small, Certain Steps Beat Big, Uncertain Leaps

You don’t need a windfall to change your future. You need a system you’ll follow on your busiest day. When in doubt, reduce friction, automate the next $10, and protect your peace of mind. Over time, saving and investing turn from chores into freedom engines—quiet, steady, and completely yours.

Note: This guide is educational, not financial advice. Your situation is unique; consider speaking with a qualified professional before making major decisions.