Private Credit vs High Yield Bonds: Best Fit for a 2025 Income & Diversification Strategy

Private Credit vs High Yield Bonds often sparks debate among fixed‑income investors building their 2025 portfolios. In today’s uncertain markets, choosing the right income‑generating asset requires balancing higher yields, liquidity, and risk control. This comprehensive guide explains how both instruments work, what drives their returns, what risks really matter, and how each can fit within a modern, income‑focused allocation. We’ll compare structures, fees, volatility, liquidity, tax considerations, and implementation paths—then finish with checklists, sample allocation frameworks, and FAQs so you can act confidently. This is educational content, not financial advice.

Understanding the mechanics of Private Credit vs High Yield Bonds starts with the fundamentals of each instrument.

1. Private Credit vs High Yield Bonds: What Is Private Credit?

Private credit—also called private debt or direct lending—is lending that occurs outside public bond markets. It typically finances privately held or mid‑sized companies through negotiated loans that do not list on an exchange. Investors provide capital to a manager (or vehicle) who originates, underwrites, and services loans directly with borrowers. Because transactions are private, terms can be customized: covenants, collateral packages, amortization, call protection, and pricing grids are all negotiated rather than standardized. Many loans are floating rate, with coupons set as a spread over a reference rate; floors are common to protect the lender if reference rates fall. Returns in private credit generally come from interest income (cash yield), upfront fees, prepayment penalties, and sometimes equity kickers such as warrants. The asset class spans multiple strategies: senior secured direct lending, unitranche loans that combine senior and junior risk into a single tranche, asset‑based loans secured by receivables or inventory, mezzanine debt with higher coupons and potential PIK features, and specialty finance such as equipment leasing or consumer credit.

Why have investors gravitated to private credit? First, bank retrenchment and tighter capital rules have limited traditional middle‑market lending capacity. Non‑bank lenders stepped in to fill the gap, often commanding an illiquidity premium—investors accept capital lockups and limited secondary markets in exchange for higher spreads. Second, floating‑rate structures align income with interest‑rate regimes: when short‑term rates are elevated, coupons adjust upward, supporting attractive yields without taking as much duration risk as fixed‑rate bonds. Third, the underwriting model gives managers more control. They can negotiate covenants, receive detailed borrower information, and intervene early if performance deteriorates. However, this control comes with responsibility: manager skill, workout experience, and sector expertise materially influence results.

Private credit risks are different from public‑market risks. Illiquidity is paramount—capital is typically locked for years, redemptions are restricted, and secondary markets may be shallow or absent. Valuations are periodic and model‑based, so mark‑to‑market volatility looks muted, but true economic risk still exists. Idiosyncratic borrower default risk can be higher because many issuers are smaller, less diversified businesses. Vintage risk matters too: loans originated during looser underwriting cycles can underperform. Leverage at the fund level can amplify both returns and losses. Finally, documentation risk is real—weak covenants or loose collateral definitions can reduce recoveries in stress scenarios.

Access pathways vary by investor type. Institutions and accredited investors may commit to closed‑end funds, SMAs, or private partnerships that call capital over a multi‑year investment period. Individual investors often access the space through Business Development Companies (BDCs), interval funds that offer quarterly liquidity with caps, or listed vehicles and ETFs that hold registered BDCs or public‑reporting debt. Every path carries trade‑offs in fees, transparency, liquidity, and governance. Cost structures generally include a management fee on committed or invested capital and a performance fee above a hurdle; some vehicles net these fees into published yields while others report gross figures, so apples‑to‑apples comparison requires care.

2.Private Credit vs High Yield Bonds: What Are High Yield Bonds?

High‑yield bonds are publicly issued corporate bonds rated below investment grade by major rating agencies. They compensate investors for elevated default probabilities with higher coupons than investment‑grade bonds. Unlike bespoke private loans, high yield bonds are standardized securities issued via syndication and traded in public markets with daily pricing. Because they are typically fixed‑rate, they carry duration exposure: when market yields rise, bond prices fall, and vice versa. While spreads reflect issuer‑specific and macro risks, the public market’s depth enables active trading, price discovery, and broad index coverage.

The high‑yield universe spans diverse sectors—communications, energy, healthcare, consumer, materials, and technology—and a ladder of ratings from BB (higher quality within high yield) to B and CCC (riskier). Default cycles tend to be clustered during economic slowdowns or refinancing waves; recoveries depend on capital structure seniority and asset coverage. Investors can access exposure through individual bonds, mutual funds, ETFs, and target‑maturity vehicles. Funds publish daily NAVs, distribute income monthly or quarterly, and allow redemptions per prospectus—features that make high‑yield attractive for investors needing flexible liquidity.

Key risks in high yield include credit risk (downgrades and defaults), interest‑rate risk (via duration), liquidity risk during market stress when bid‑ask spreads widen, and sector‑specific shocks such as commodity volatility or regulatory changes. However, the public nature of the market enhances transparency: audited financials, earnings calls, and real‑time pricing flows into valuation quickly, enabling risk management via diversification and hedging.

3. Side‑by‑Side Comparison: Private Credit vs High Yield Bonds

A clear side‑by‑side comparison helps translate features into portfolio implications. Below is a practical lens across five dimensions that matter most to investors in 2025.

When comparing Private Credit vs High Yield Bonds, liquidity and risk profiles vary significantly.

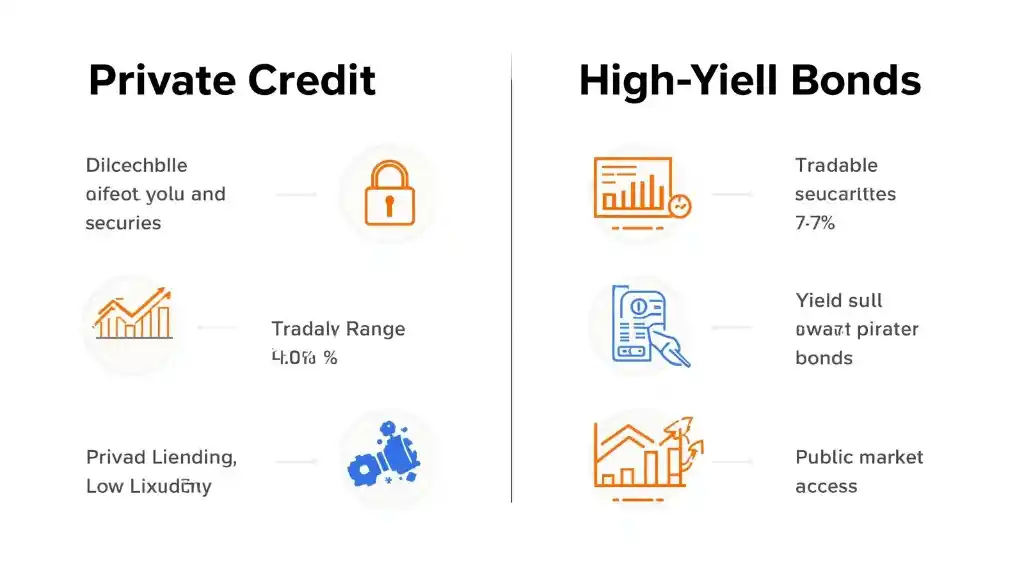

Private Credit vs High Yield Bonds: Liquidity

Private Credit: Low liquidity; multi‑year lockups; redemptions limited; secondary markets thin.

High‑Yield Bonds: High relative liquidity; daily pricing; ETFs and funds enable subscriptions/redemptions.

Private Credit vs High Yield Bonds: Yield Potential

Private Credit: Typically higher cash yields due to illiquidity premium and negotiated spreads; many loans are floating‑rate with floors.

High‑Yield Bonds: Elevated yields versus investment‑grade but often below private credit; mostly fixed‑rate.

Private Credit vs High Yield Bonds: Volatility & Valuation

Private Credit: Lower apparent volatility because marks are periodic; economic risk remains and shows up through write‑downs or realized losses.

High Yield Bonds: Mark‑to‑market daily; prices move with risk sentiment and rates, which increases headline volatility but enables tactical rebalancing.

Private Credit vs High Yield Bonds: Risk & Recovery

Private Credit: Frequently senior secured with covenants; recovery outcomes depend on documentation and collateral quality.

High Yield Bonds: Often unsecured or subordinated within capital structures; recoveries vary and can be lower in deep downturns.

Private Credit vs High Yield Bonds: Transparency & Access

Private Credit: Opaque loans; manager reporting varies; often limited to accredited or institutional channels.

High Yield Bonds: Public disclosures, broad analyst coverage, regulated fund structures, and accessible ETFs/mutual funds.

4. The 2025 Backdrop: Rates, Refinancing, and Dispersion

The 2025 backdrop is defined by dispersed outcomes and still‑elevated short‑term rates relative to the pre‑2022 era. For private credit, floating coupons translate into robust cash yields when reference rates remain high, but refinancing tests borrowers’ free cash flow and pricing power. For high yield, the key balancing act is the trade‑off between attractive carry and sensitivity to rates: duration can detract if yields rise further, yet price upside exists if rates drift lower and spreads remain contained.

Another theme is the refinancing wall for sub‑investment‑grade issuers whose debt matures over the next few years. Stronger credits can refinance in public markets at higher coupons; weaker credits may turn to private lenders where documentation flexibility is greater but covenants are tighter. This segmentation can reward careful underwriting in private credit and quality tilts (e.g., BB focus) in high‑yield portfolios.

A final consideration is dispersion across sectors and ratings. Energy, healthcare services, and software may face idiosyncratic pressures unrelated to macro rates. Managers with robust sector teams and active workout capabilities can exploit dispersion through security selection, while index investors can mitigate single‑name risk via broad diversification.

Building a diversified fixed income sleeve requires analyzing Private Credit vs High Yield Bonds trade-offs carefully.

5. How to Use Private Credit vs High Yield Bonds in Your Portfolio

How do you translate the differences into a portfolio? Here are three archetypes to consider—these are illustrative frameworks, not recommendations.

Income‑First Core: Investors prioritizing steady cash flow might allocate a larger sleeve to private credit for higher coupons, complemented by high‑yield ETFs for daily liquidity. A 60/40 split within the non‑investment‑grade sleeve (60% private credit vehicles; 40% high‑yield funds) can combine income with an instant liquidity buffer. Periodic rebalancing harvests volatility from the public sleeve while leaving the private sleeve to compound.

Balanced Barbell: For investors seeking resilience, pair senior secured direct lending (more defensive within private credit) with upper‑tier high‑yield (BB/strong B). The barbell targets downside protection on one end and tradable flexibility on the other, with tactical tilts added around rate moves or spread changes.

Opportunistic Satellite: More advanced allocators can use a core high‑yield fund for liquidity and add niche private credit sleeves—asset‑based lending, specialty finance, or stressed/distressed—when underwriting skill and entry pricing look favorable. Position sizing is key because dispersion is high and manager selection dominates outcomes in niche strategies.

6. Risk‑Management Checklists

Before allocating, use a structured risk‑management checklist. For private credit managers:

– Strategy definition: senior secured, unitranche, mezzanine, specialty finance?

– Origination edge: proprietary sourcing, sponsor relationships, repeat borrowers?

– Underwriting discipline: leverage thresholds, interest coverage, covenant packages, collateral valuation standards?

– Portfolio construction: issuer caps, sector limits, geography, and vintage diversification?

– Workout capability: in‑house restructuring expertise, historical recovery rates, legal documentation strength?

– Liquidity terms: lockup length, gates, redemption mechanics, and secondary options?

– Fees and alignment: management/performance fee levels; GP co‑investment; hurdle and clawback terms?

For high‑yield funds and ETFs:

– Duration profile and rate sensitivity; use of derivatives for hedging?

– Credit quality mix across BB/B/CCC; historical drawdown behavior?

– Cost: expense ratio and trading friction (bid‑ask spreads) for ETFs?

– Liquidity profile under stress: creation/redemption mechanisms; use of cash buffers or lines of credit?

– Tracking error versus benchmark; active share for active funds?

7. Taxes and Account Location (US/UK Overview)

Taxes and account location matter. In general, interest from both private credit and high‑yield bond funds is taxed as ordinary income in many jurisdictions. Investors in the United States often prefer to hold income‑heavy assets in tax‑advantaged accounts (IRAs, 401(k)s) where possible; in the United Kingdom, wrappers like ISAs and SIPPs can shelter distributions and capital gains, subject to specific rules. Tax rules are complex and situational—consult a qualified tax adviser for guidance tailored to your circumstances. Also check whether your vehicle reports income as ordinary interest, qualified dividends, or return of capital, as each has different implications.

8. Implementation Paths & Costs

Implementation choices shape your lived experience as an investor. Private credit access vehicles include closed‑end drawdown funds, evergreen private funds with periodic subscriptions, BDCs (listed and non‑traded), and interval funds. Drawdown funds call capital over time and distribute repayments; evergreen vehicles smooth cash flows through subscription and redemption windows; BDCs provide transparency via periodic public reports; interval funds offer limited quarterly liquidity. Each has different reporting cadences, valuation practices, and investor protections.

Public high‑yield exposure can be implemented via large, liquid ETFs that track broad indices, actively managed mutual funds that aim to outperform through security selection, or custom ladders of individual bonds for investors with larger accounts. Active managers may tilt quality, sector, and duration through cycles, while ETFs offer low cost and intraday tradability. Costs are not just expense ratios—consider trading spreads, redemption fees, and, in private vehicles, performance‑fee arrangements that affect net yield.

9. FAQs

Frequently asked questions help clarify practical concerns:

Q1) Which is better for a rising‑rate environment?

- A) Private credit’s floating‑rate coupons can reset higher as reference rates rise, while fixed‑rate high‑yield bonds face price pressure from duration. However, if rates fall, fixed‑rate bonds can deliver price gains; floating‑rate income may reset lower.

Q2) How do I think about default risk?

- A) In private credit, security packages and covenants can mitigate loss severity, but borrower size and transparency are lower. In high‑yield, diversified funds spread single‑issuer risk across hundreds of names, but recoveries vary widely across sectors and cycles.

Q3) Can I get diversification benefits from holding both?

- A) Yes. Private credit’s valuations move more slowly, dampening headline volatility, while high‑yield’s daily pricing allows tactical rebalances. Income streams and risk drivers are related but not identical.

Q4) What position size is sensible?

- A) Many investors size non‑investment‑grade income sleeves within a broader fixed‑income allocation, then divide that sleeve between private and public credit based on liquidity needs, risk tolerance, and access.

Q5) What’s the biggest mistake new allocators make?

- A) Underestimating illiquidity and overestimating the ability to exit private vehicles during stress. Second‑order issues include ignoring fund‑level leverage, accepting loose covenants, or chasing headline yields without evaluating underwriting quality.

Q6) Can I combine Private Credit vs High Yield Bonds in the same portfolio?

- A) Yes. Many investors blend Private Credit vs High Yield Bonds to optimize for both yield and flexibility. While private credit offers higher potential income, high-yield bonds provide daily liquidity and transparency.

10. Pros and Cons Summary

Pros of Private Credit:

– Higher potential cash yields driven by illiquidity premium and negotiated spreads.

– Floating‑rate coupons reduce duration risk and can hedge inflationary periods.

– Covenant control, collateral, and direct information access support proactive risk management.

– Lower day‑to‑day price volatility because valuations are periodic rather than continuous.

Cons of Private Credit:

– Illiquidity and lockups; secondary markets may be thin or unavailable.

– Manager selection and documentation quality are critical; dispersion in outcomes is wide.

– Valuation lags can obscure deteriorating fundamentals until marks catch up.

– Fees can be higher, especially in performance‑fee structures.

Pros of High‑Yield Bonds:

– Daily liquidity, transparent pricing, and broad access via ETFs and funds.

– Diversification across sectors and issuers; ease of portfolio rebalancing.

– Potential price appreciation if rates fall or spreads compress.

Cons of High‑Yield Bonds:

– Mark‑to‑market volatility; sensitive to macro risk sentiment and rate moves.

– Generally lower yields than private credit for comparable risk levels.

– Recoveries can be lower in unsecured parts of the capital structure.

Conclusion

Private credit can boost portfolio income and dampen headline volatility, but it demands patience, careful manager selection, and acceptance of illiquidity. High‑yield bonds add flexibility and transparency, enabling tactical changes and daily liquidity, albeit with more visible price swings. For many investors in 2025, the right answer is not either/or but both: a blended sleeve that matches your liquidity needs, time horizon, and risk tolerance.

Next Steps:

– Map your 12–36 month liquidity needs before committing to illiquid vehicles.

– Decide whether you prefer active security selection or low‑cost index exposure in the public sleeve.

– Build a shortlist of private credit managers and vehicles; scrutinize underwriting standards, fees, and workout history.

– Start with modest position sizes; scale only after observing how distributions, reporting, and volatility behave through a few quarters.

– Revisit the allocation quarterly to incorporate changes in rates, spreads, and personal cash‑flow needs.

This is educational content, not financial advice.

11. Scenario Analysis & Stress Testing

A disciplined allocator does not rely on base‑case expectations alone. Scenario analysis helps translate macro uncertainties into practical portfolio decisions.

Consider three simplified scenarios for 2025–2026 and how each sleeve might behave:

• Soft‑Landing: Growth slows but remains positive, inflation trends lower, and policy rates decline gradually. High‑yield bonds may enjoy price appreciation from duration and spread stability, while private credit’s floating coupons reset modestly lower yet still deliver robust cash income. Rebalancing from bonds that rally into private credit can maintain your target yield.

• Reacceleration: Growth re‑heats, inflation proves sticky, and policy rates stay higher for longer. Private credit’s floating coupons continue to pay elevated cash yields, but borrowers’ interest burdens rise; underwriting discipline and covenant enforcement become crucial. High‑yield bond prices may tread water as higher rates offset carry; focusing on shorter duration and higher quality can help.

• Hard‑Landing: A profits recession lifts defaults. Public high‑yield marks down quickly; losses are visible in real time, but selective opportunities emerge for active buyers. Private credit funds mark down more slowly and intensify workouts; collateral and covenants influence recoveries. Liquidity becomes precious—this is where sizing and cash buffers in the public sleeve matter most.

Stress testing should not be a one‑time exercise: revisit assumptions quarterly and ask how your allocation behaves if spreads widen 200–300 bps, if short‑term rates fall 150 bps, or if redemptions hit your public funds during a shock. The goal is not to predict the future but to be prepared for a range of plausible paths.

12. Example Implementation Playbooks (US & UK)

Playbook A – U.S. Tax‑Deferred Focus: An investor with access to a 401(k) and IRA prioritizes tax efficiency. Place high‑yield funds and BDC/interval‑fund exposure inside tax‑advantaged accounts to defer taxation on ordinary income. Use a broad, low‑cost HY ETF (core) plus an actively managed HY fund (satellite) for selection alpha. Add a modest private credit interval fund allocation sized to your tolerance for limited liquidity.

Playbook B – U.K. ISA/SIPP Wrapper: A long‑term saver utilizes ISA and SIPP accounts. Hold a BB‑tilted HY fund within the ISA for monthly income and reinvest distributions. Allocate a measured slice to private credit via a listed BDC or an authorized fund that fits SIPP rules, mindful of ongoing charges and dealing spreads. Review the cost disclosures and look‑through holdings where possible.

Playbook C – Liquidity‑Sensitive Professional: A freelancer with variable income needs the option to raise cash quickly. Emphasize public high‑yield ETFs for the majority of the income sleeve and restrict private credit exposure to vehicles with clearly disclosed quarterly windows and conservative gates. Maintain a three‑to‑six‑month cash reserve in T‑bills or money‑market funds separate from the non‑investment‑grade allocation.

Each playbook should be customized. Think in “layers”: outer layer = emergency cash and short‑duration reserves; middle layer = liquid public credit; inner layer = long‑term private credit. The deeper the layer, the longer the lockup and the higher the expected yield, with position sizes reflecting your personal cash‑flow map.

13. Fee Math & Net‑of‑Fee Reality Checks

Headline yields can be seductive, but net‑of‑fee outcomes pay the bills. In private credit, a 1–1.5% management fee plus performance fees above a hurdle can reduce distributable yield meaningfully; check whether fees are charged on committed or invested capital. Ask managers to show net IRR and net cash‑on‑cash under realistic default and recovery assumptions.

For public high‑yield, expense ratios are visible, but trading spreads and market‑impact costs also matter, especially for smaller funds or stressed periods. Active funds deserve their fees only if they deliver better risk‑adjusted returns than passive alternatives through cycles. Compare five‑year drawdowns, not only one‑year returns. Finally, watch leverage at both vehicle and portfolio levels—borrowing can boost yields in good times and magnify losses when spreads gap wider.

14. Governance, Reporting, and ESG Considerations

Governance quality often separates durable managers from fair‑weather lenders. Review board composition, audit practices, valuation committees, and third‑party pricing checks. Transparent monthly or quarterly reporting that includes cohort performance, non‑accrual rates, and realized loss metrics enables informed oversight.

Some investors incorporate ESG screens or engagement practices. In private credit, lender influence can shape borrower behavior through covenants on disclosure, safety, or environmental policies; in public markets, investors can express preferences through fund mandates that exclude certain sectors or emphasize better‑rated issuers. ESG is not a substitute for credit work, but it can identify risk externalities before they become headline problems.

15. Putting It All Together

A practical rule of thumb: start with your liquidity map, build outward from the safest layer, and let the allocation to private credit grow only as you gain confidence with the vehicle’s behavior. If you need the ability to rebalance monthly, overweight high‑yield funds. If you are comfortable with multiyear capital commitments and want higher, floating cash income, allocate a measured portion to private credit. Document your thesis, target weights, and rebalance bands today—before markets force decisions under pressure.

The comparison between private credit and high‑yield bonds is not about crowning a permanent winner. It is about recognizing different engines of return and choosing the mix that aligns with your constraints. Manage what you can control: costs, position sizes, diversification, and behavior. The rest—rates, spreads, and cycles—will always be uncertain. Preparation, not prediction, is the durable edge.

Ultimately, Private Credit vs High Yield Bonds is not about choosing one over the other, but finding the right blend for your goals.

Further Reading on Private Credit and High Yield Bonds

- Investopedia – What Are High Yield Bonds?

- Investopedia – Private Credit Overview

- S&P Global Ratings – Credit Market Research

- Federal Reserve – Monetary Policy Tools

- U.S. SEC – Public Disclosures and Bond Filings