If you care about what you actually keep, not just what you earn, tax-efficient investing is your unfair advantage. Markets can be loud and fickle; taxes are quiet and persistent. Two portfolios with the same pre-tax return can end miles apart after taxes. This guide is your practical playbook for turning that gap into real money you keep—without turning your life into spreadsheets.

Here’s the core idea: design your portfolio so every decision—what you buy, where you hold it, when you sell—leans toward higher after-tax returns. That means using structures that naturally minimize taxable distributions (think broad-market ETFs), techniques that capture losses without derailing your strategy (tax-loss harvesting), and rules-of-thumb that keep you out of trouble (wash-sale awareness, lot selection, and smart rebalancing).

You don’t need exotic products or heroic timing. You do need a repeatable system. In 2025, that system often blends low-turnover index ETFs for the core with selective tools—like direct indexing—when you want tighter control over realized gains and losses in taxable accounts. The goal isn’t to dodge taxes forever; it’s to defer, reduce, and smooth them so compounding does the heavy lifting.

By the end of this guide, you’ll be able to:

Compare ETFs, mutual funds, and direct indexing through an after-tax lens.

Apply tax-loss harvesting without triggering wash-sale surprises.

Decide when simplicity (ETF core) beats complexity (full direct indexing).

Build a year-round workflow that automates the boring parts and documents the important ones.

A quick word on scope: this playbook focuses on US taxpayers using taxable brokerage accounts. We’ll touch on account “location” and rebalancing, but retirement accounts (IRAs/401(k)s) behave differently and deserve their own deep dive. Also, we’ll keep the math clean and the examples illustrative rather than hyper-customized.

If you’re an intermediate investor, you already know the basics of broad diversification and costs. Consider this your next power-up: align structure, behavior, and rules so the IRS takes only what it must—and no more. Ready? Let’s map the 2025 tax landscape you’re actually investing in.

Education only: This is educational content, not financial advice.

The 2025 Tax Landscape—What Actually Matters

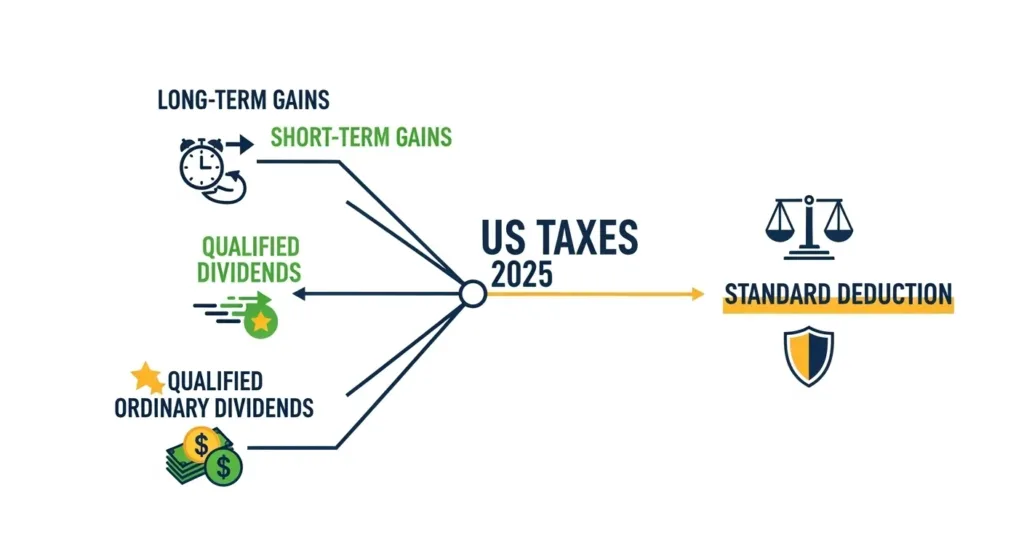

Long-Term vs. Short-Term Capital Gains

Long-term capital gains (assets held over 1 year) and qualified dividends are taxed at 0%, 15%, or 20%, depending on your taxable income and filing status. Short-term gains (≤1 year) are taxed as ordinary income at your marginal rate. Thresholds adjust annually for inflation; for 2025, published ranges place the 20% rate at higher incomes, while most investors fall into the 0% or 15% bands. Always check the current IRS thresholds when planning sales.

Why it matters: realizing gains after the one-year mark can meaningfully lower your tax bill; pairing long-term holding with selective harvesting helps smooth taxable income across years.

Qualified vs. Ordinary Dividends

Dividends come in two flavors. Qualified dividends (meeting IRS requirements on holding period and issuer) are taxed at the favorable capital-gains rates above. Ordinary (non-qualified) dividends are taxed at your regular income rates. Your Form 1099-DIV labels these categories; plan around record dates and holding-period rules to preserve “qualified” status.

Why it matters: chasing yield without checking its “qualified” mix can raise your effective tax drag even if headline yields look similar.

The Standard Deduction (Context for Planning)

For tax year 2025, the IRS standard deduction is $15,000 (single/MFS), $22,500 (HOH), $30,000 (MFJ/QSS), indexed for inflation; recent legislation and inflation adjustments have also been discussed widely in financial media. These amounts shape your taxable income and can influence whether some LTCG/qualified dividends fall into the 0% bracket.

Why it matters: location decisions (which assets sit in taxable vs. tax-advantaged accounts) interact with your deduction and brackets; smart placement can push more of your gains/dividends into lower rates.

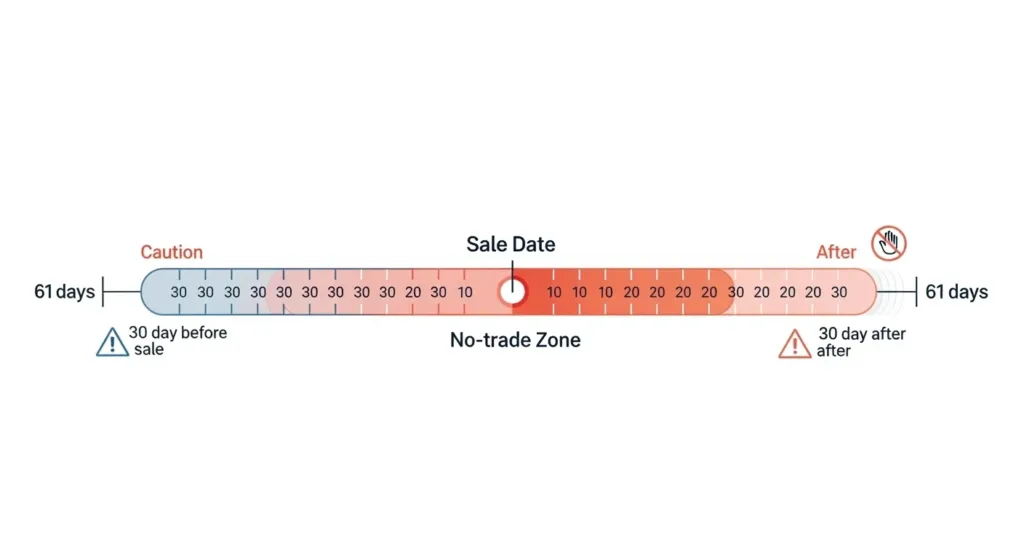

The Wash-Sale Rule (Guardrails for Harvesting)

When you sell a security at a loss, you cannot claim that loss if you buy a “substantially identical” security within 30 days before or after the sale; the disallowed loss gets added to the basis of the new shares, effectively postponing the deduction. Turn off DRIPs around harvests, use clearly different substitutes, and document lots to stay compliant.

Why it matters: tax-loss harvesting boosts after-tax returns only if the losses are allowed. Good hygiene—timing, substitutes, and lot tracking—keeps the benefit intact.

Bottom line: 2025 rules still reward long-term holding, qualified dividends, and careful harvesting. Know your brackets, preserve qualified status, and respect wash-sale timing to keep more of each dollar compounding.

Why ETFs Tend to Win on Taxes (and supercharge Tax-Efficient Investing)

Broad-market ETFs have a structural edge: they can meet redemptions in-kind, handing out securities to authorized participants instead of selling positions and realizing gains. That’s the quiet engine behind Tax-Efficient Investing for taxable accounts.

How the ETF mechanism reduces taxable distributions

ETFs use a creation/redemption process with authorized participants; mispricings are arbitraged, and—crucially—redemptions can be done in-kind, which helps avoid distributing capital gains to shareholders. See a plain-English explainer on the creation/redemption mechanism here:Investopedia and a deeper ETF overview here: SEC Investor Bulletin (PDF). For Tax-Efficient Investing, that structural choice often translates into fewer surprise year-end payouts.

When ETFs shine vs. mutual funds

Because mutual funds typically sell securities to meet redemptions, they’re more likely to realize gains that get passed through to investors. By contrast, diversified core equity ETFs have historically shown lower capital-gain distributions on average. For a data-driven perspective, see Morningstar’s analysis: “Capital Gains Distributions Remain Low” and their 2025 picks for tax-efficiency:Morningstar list. This is a cornerstone of Tax-Efficient Investing.

Important nuance: not every ETF is magically tax-free

ETFs can still distribute gains in certain cases (complex/derivatives strategies, portfolio changes, or unusual flows). See a recent real-world example covered by Barron’s: case study. Structure helps, discipline seals the deal—Tax-Efficient Investing still requires thoughtful fund selection and holding periods.

Dividend quality still matters

Qualified dividends generally get capital-gains rates if you meet the holding-period rules (commonly 61 days within a 121-day window around the ex-dividend date). Quick refreshers: Vanguard explainer and Fidelity guide. Pairing qualified-dividend awareness with ETFs strengthens Tax-Efficient Investing.

Takeaway: ETFs aren’t magic, but their in-kind plumbing and low turnover make them the default chassis for Tax-Efficient Investing in taxable accounts—then you layer in holding-period discipline and smart harvesting to keep more of every dollar compounding.

Direct Indexing—Tax Control for Taxable Accounts (for stronger Tax-Efficient Investing)

Direct indexing lets you hold the underlying stocks of an index instead of an ETF or mutual fund. That granular control helps you realize losses, defer gains, and fine-tune income—core levers of Tax-Efficient Investing in a taxable brokerage account.

How direct indexing works (quick tour)

You replicate a broad index (e.g., S&P 500) by owning many of its individual names.

Software scans positions daily for harvestable losses and places replacement stocks or sector proxies.

You can set guardrails (tracking-error limits, turnover caps) to keep performance close to the target index. This precision supports Tax-Efficient Investing because you’re managing taxes at the security level, not just at the fund level.

Why it can boost after-tax returns

Systematic tax-loss harvesting (TLH): Harvest small losses across many names throughout the year, even in flat or up markets.

Gain deferral: Choose which lots to sell and when, nudging more gains into long-term territory.

Dividend control: Tilt away from non-qualified dividend payers if desired (within tracking-error limits). Used thoughtfully, these techniques reinforce Tax-Efficient Investing by reducing annual tax drag while preserving market exposure.

Trade-offs to keep in mind

Complexity: More moving parts than a one-fund ETF core.

Costs: Management fees and trading frictions (though many platforms offer commission-free trading).

Tracking error: You won’t match the index perfectly, especially with restrictions (ESG screens, concentration limits).

Wash-sale management: Need careful substitutes and DRIP controls to keep harvested losses valid. These are not deal-breakers, but they mean Tax-Efficient Investing with direct indexing works best for larger taxable balances and investors comfortable with light oversight.

Simple workflow (repeatable)

Define the target index and acceptable tracking-error band.

Automate TLH scans (daily/weekly), with pre-approved replacement lists.

Set lot-selection rules (HIFO/Specific ID) at the custodian level.

Turn off DRIPs for harvest-eligible tickers around key dates.

Quarterly check-ins: review realized gains, harvested losses, and tracking error. This playbook keeps Tax-Efficient Investing systematic, not improvisational.

Example (illustrative, simplified)

Portfolio replicates 400+ names of a broad US index.

In a choppy quarter, 35 positions show small unrealized losses; the system sells them and swaps to pre-vetted alternatives in the same industries.

Net: $7,500 in harvested losses to offset current gains and up to $3,000 of ordinary income (carry the rest forward). Mechanically ordinary, but cumulatively powerful for Tax-Efficient Investing.

Education only: This is educational content, not financial advice.

The Wash-Sale Rule (keep your Tax-Efficient Investing clean)

The wash-sale rule disallows a capital loss if you buy a “substantially identical” security within 30 days before or after selling it for a loss. The disallowed loss isn’t gone—it’s added to the cost basis of the replacement shares—so the benefit is deferred, not denied. Respecting this rule is non-negotiable for reliable Tax-Efficient Investing.

What “substantially identical” usually means

Individual stocks: Ticker A vs. the same ticker A is clearly identical. Ticker A vs. a close peer (same industry) is not identical.

ETFs & index funds: Two funds tracking the same index are risky (e.g., S&P 500 ETF vs. another S&P 500 ETF). Funds tracking highly overlapping but different indexes (e.g., S&P 500 vs. Total Market) are typically used as harvest pairs, but document the rationale.

Options/DRIPs: Buying calls, exercising employee stock, or auto-reinvesting dividends (DRIP) can trigger wash sales across accounts.

The 61-day danger zone

Think of it as a 61-day window: 30 days before the loss sale, the trade date, and 30 days after. Purchases anywhere in that span—even in an IRA or a spouse’s account—can cause a wash sale. For bulletproof Tax-Efficient Investing, coordinate across all accounts.

Practical anti-wash workflow

Turn off DRIPs on harvest-eligible holdings (temporarily around ex-dates).

Block “repurchase” rules in your rebalancer for 30+ days.

Use Specific ID/HIFO at the broker so you control which lots are sold.

Keep an audit trail: screenshots, trade confirmations, and a brief note on why the substitute isn’t substantially identical.

Simple example (timeline)

Day 0: Sell ABC ETF (tracks S&P 500) at a $2,400 loss.

Day 0: Buy VTI-like exposure (total-market) as the substitute.

Days 1–30: No purchases of S&P 500-tracking funds; DRIPs off.

Day 31+: You may rotate back if desired. Result: loss is allowed; your market exposure stayed similar—clean Tax-Efficient Investing.

Basis adjustment in plain English

If you accidentally trigger a wash sale, the disallowed loss is added to the basis of the replacement lot and the holding period tacks to the new shares. You didn’t “lose” the loss; you postponed it. Still, the delay weakens near-term tax alpha—so prevention beats cure.

Good harvest pairs (illustrative, not endorsements)

US large-cap S&P 500 ↔ US total-market broad index

US growth large-cap ↔ US large-cap blend

Developed ex-US broad index ↔ all-world ex-US These pairings keep tracking error modest while lowering “identical” risk—useful for Tax-Efficient Investing without tripping wires.

Education only: This is educational content, not financial advice.

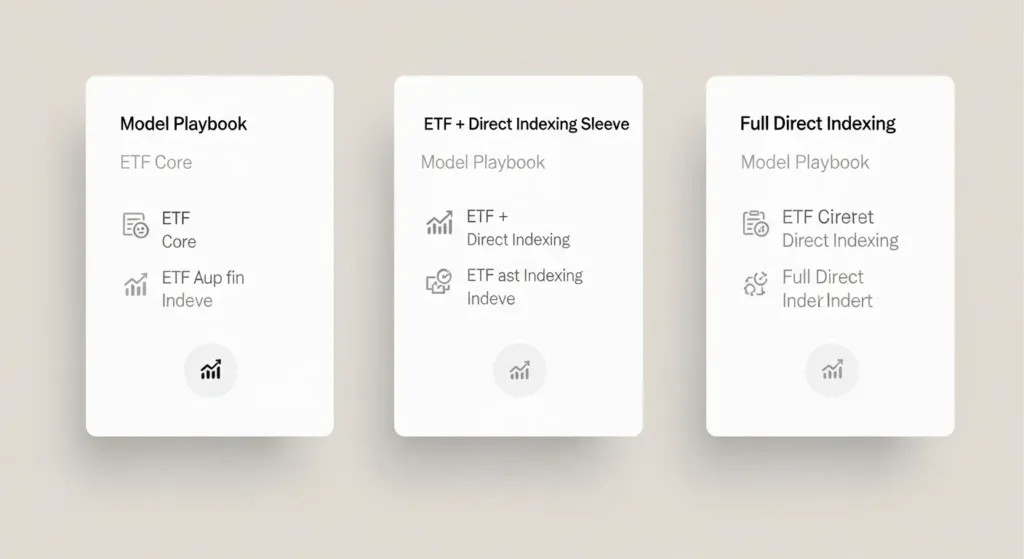

Putting It Together — Three Model Playbooks (2025)

1) Set-and-Simplify (ETF Core)

Who it’s for: Busy investors who want low-maintenance Tax-Efficient Investing with broad exposure. Core: 2–4 low-turnover index ETFs (US total market, international, bonds). Rules:

Automatic contributions monthly; rebalance at 5% bands or annually.

Specific-ID/HIFO at the broker; DRIPs on for bond funds, off for equities near harvest windows.

Opportunistic tax-loss harvesting (TLH) only when losses exceed a threshold (e.g., $1,000 per asset). Outcome: Minimal distributions, simple records, dependable Tax-Efficient Investing.

2) The Optimizer (ETF Core + Targeted Direct Indexing)

Who it’s for: Investors with sizable taxable balances who still value ETF simplicity. Core: ETF backbone (US/international) + a direct-index sleeve for US large-cap. Rules:

Daily/weekly TLH scans on the DI sleeve; quarterly on ETFs.

Tracking-error guardrail (e.g., ≤1.5% vs. target index).

Capital-gain budget per year (e.g., realize ≤$X short-term; prefer long-term). Outcome: Higher loss capture while keeping the portfolio manageable—balanced, practical Tax-Efficient Investing.

3) Full Direct Indexing (DI Core)

Who it’s for: High-income investors prioritizing custom TLH, factor tilts, or ESG screens. Core: DI across US equities, with ETFs for small niches (intl/small caps). Rules:

Automated TLH with pre-approved substitutes; DRIPs off on equity sleeve.

Lot-level gain deferral playbook (long-term bias).

Monthly tracking-error review; tighten if markets trend strongly. Outcome: Maximum control over realized gains/losses; record-keeping and oversight required to keep Tax-Efficient Investing clean.

Direct indexing platforms: Index replication, substitute lists, TE guardrails.

Tax/lot software: Dashboards for unrealized P/L, harvest rules, audit trails.

Index tracking tools: Monitor TE vs. target.

FAQs

Are ETFs always more tax-efficient than mutual funds? Usually for broad equity exposure, yes—but strategy matters.

When is direct indexing worth it? With large taxable balances, concentrated positions, or when you want granular TLH and constraints (e.g., ESG).

How do I avoid wash-sales while harvesting? Turn off DRIPs, use non-identical substitutes, and block repurchases for 30+ days.

Do long-term gains always beat short-term? Rates are generally lower, but decisions depend on your bracket, state taxes, and total income.

Where should “tax-inefficient” assets go? Prefer tax-advantaged accounts; keep broad, low-turnover equity ETFs in taxable.

Cookie Consent

We use cookies to improve your experience on our site. By using our site, you consent to cookies.

This website uses cookies

Websites store cookies to enhance functionality and personalise your experience. You can manage your preferences, but blocking some cookies may impact site performance and services.

Essential cookies enable basic functions and are necessary for the proper function of the website.

Name

Description

Duration

Cookie Preferences

This cookie is used to store the user's cookie consent preferences.

30 days

These cookies are needed for adding comments on this website.

Name

Description

Duration

comment_author

Used to track the user across multiple sessions.

Session

comment_author_email

Used to track the user across multiple sessions.

Session

comment_author_url

Used to track the user across multiple sessions.

Session

Statistics cookies collect information anonymously. This information helps us understand how visitors use our website.

Google Analytics is a powerful tool that tracks and analyzes website traffic for informed marketing decisions.

Contains information related to marketing campaigns of the user. These are shared with Google AdWords / Google Ads when the Google Ads and Google Analytics accounts are linked together.

90 days

__utma

ID used to identify users and sessions

2 years after last activity

__utmt

Used to monitor number of Google Analytics server requests

10 minutes

__utmb

Used to distinguish new sessions and visits. This cookie is set when the GA.js javascript library is loaded and there is no existing __utmb cookie. The cookie is updated every time data is sent to the Google Analytics server.

30 minutes after last activity

__utmc

Used only with old Urchin versions of Google Analytics and not with GA.js. Was used to distinguish between new sessions and visits at the end of a session.

End of session (browser)

__utmz

Contains information about the traffic source or campaign that directed user to the website. The cookie is set when the GA.js javascript is loaded and updated when data is sent to the Google Anaytics server

6 months after last activity

__utmv

Contains custom information set by the web developer via the _setCustomVar method in Google Analytics. This cookie is updated every time new data is sent to the Google Analytics server.

2 years after last activity

__utmx

Used to determine whether a user is included in an A / B or Multivariate test.

18 months

_ga

ID used to identify users

2 years

_gali

Used by Google Analytics to determine which links on a page are being clicked

30 seconds

_ga_

ID used to identify users

2 years

_gid

ID used to identify users for 24 hours after last activity

24 hours

_gat

Used to monitor number of Google Analytics server requests when using Google Tag Manager